The general definition of accounting is something like:

“the collection, registration, aggregation and reporting of financial transactions in companies or organisations to provide the necessary information to make and evaluate financial decisions”.

As long as we live in a society with scarce resources, then non-capitalist and democratic economies organised around self-managed workplaces and neighbourhoods, will ALSO need an accounting system that generates necessary information for decision-makers, so that they can make efficient and fair decisions on resource allocation, production and income distribution. Accounting in such an economy will focus on facilitating and promoting democratic decision making, equality and solidarity, and not profits and return on private investments.

A libertarian socialist economy will have different values and institutions than a capitalist or state socialist economy regarding decision making, income distribution and ecological sustainability, but if a future libertarian socialist economy is to be democratic, fair, efficient and ecologically sustainable, it has to implement some kind of an accounting system that summarises and presents the required information to all decision makers in the economy, all affected parties that is, in a transparent and accessible way. If it fails to do so it will eventually revert into some version of the authoritarian economic systems that we want to escape.

Accounting Objectives

The main objectives for an accounting system in a participatory economy is to enable and promote:

- Planning of future economic activity in three separate planning procedures with different time horizons – long term development planning, investment planning and annual planning.

- Recording of economic transactions during the current year.

- Continuous monitoring and evaluation of outcomes in relation to plan for various activities, and possible adjustments of the current annual plan and other future plans.

In order to achieve these goals, the design of the accounting system must permit economic actors to correctly estimate, record and evaluate:

- (i) the opportunity costs of using various categories of labour, natural resources such as agricultural land and forests, and produced capital assets such as factory buildings and equipment,

- (ii) the social costs of producing and consuming various goods and services,

- (iii) the damage, or social cost of emissions of different pollutants, and

- (iv) as best possible the social rate of return on investment in expanding different aspects of the productive capacity operative over many years.

In this context there are a number of issues of a technical and practical nature to consider. One crucial issue is how all the different varieties of goods, services, capital assets, resources and emissions of polluting substances should be defined, categorised and quantified so that; a) consumers and workers can relate to them in an efficient way, b) their prices will reflect the opportunity costs of productive resources and the social costs of goods and services, c) a viable, fair and efficient annual plan will emerge in the annual planning procedure and d) an efficient monitoring of the annual plan is facilitated.

A Participatory Economy Accounting System

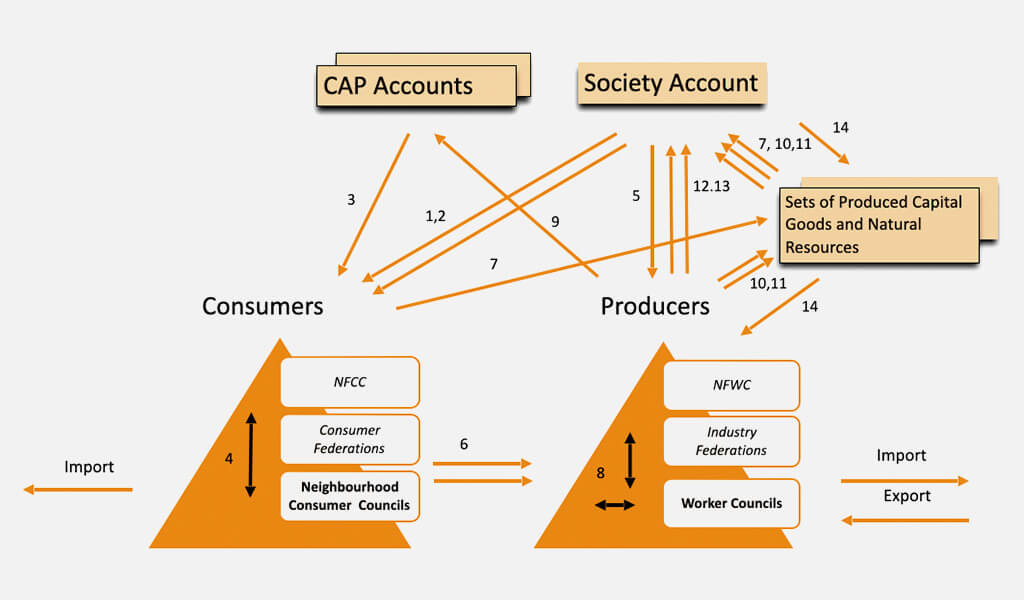

The diagram above gives an overview of a possible accounting system, or rather of the financial transactions of flows, in a participatory economy. In our accounting system, we identify two primary categories of accounting entities whose economic activities and financial transactions are tracked and recorded to facilitate efficient and fair decisions, (A) Consumers, their councils and federations, and (B) Producers, worker councils and their federations.

In addition, we introduce a separate group of accounting entities to facilitate the recording and monitoring of society’s production and use of sets of capital assets. We also introduce something called CAP Accounts, which are accounts connected to Communities of Affected Parties (CAPs), whose purpose it is to facilitate the transfer of fees that worker councils are charged for emissions of harmful pollutants to the affected parties as income. A CAP account works as a sort of reconciliation account for worker councils’ fees and members’ compensation, based on rules agreed on by the CAP.

Finally, we introduce a Society Account, which together with the CAP accounts represent society’s total GDP or its total income, which is allocated between consumption and investments.

The arrows in the flow chart indicates the flow of financial transactions.

Consumers’ income

At the aggregate level and over time, consumption in a participatory economy equals the sum of income from four sources. First, income as compensation for socially beneficial work, based on their effort ratings in their worker councils, indicated by arrow 1. Note here that the workers’ compensation for work will NOT affect their worker councils’ accounts but rather come from the society account. However, at the same time, worker councils are charged fees for their access to labour, which are decided in the annual planning procedure and should reflect labours opportunity cost. These fees become part of society’s income and is credited the society account as represented by arrow 12 in the flow chart.

The second component of consumers’ total income is their compensation from politically decided and specified national programmes, such as children, retirement and disability benefits, arrow 2 in the chart. The third source of income comes from the Communities of Affected Parties (CAPs), as compensation for the harm that the members are caused by emissions of various pollutants by worker councils, arrow 3. And finally, consumers may reallocate income between themselves based on special need requests granted by their fellow members, represented by arrow 4. One may also consider publicly funded national service programmes such as health care and education systems as a form of consumers’ income. This is represented by arrow 5 in the chart.

Consumers’ income can be considered as their claim on the “total pie” that is baked in the economy, the economy’s GDP. The greater the fraction of the total production used for investment, the less consumption, and vice versa. By estimating, before the annual planning, the value of the economy’s total consumption, deducting for the politically decided benefit programmes and compensation from CAPs, and then dividing the sum with total hours worked, a base compensation per hour worked can be calculated for the year, which can then be adjusted based on worker councils’ effort ratings.

Compensation for pollution

In a participatory economy, the polluters are charged for the harm and damage that their pollution cause and those who are affected are compensated for the harm they suffer. Communities of Affected Parties (CAP) bring together all parties that are negatively affected by a substance. The CAPs propose how much emission that they are willing to allow, considering that they will be compensated by an amount equal to the current cost estimate from the annual planning, as indicated by arrow 3 in the chart. Of course, society as a whole or any individual CAP may decide that it does not want to allow any emissions at all of a specific substance, but if a CAP accepts a certain amount of release, it will be compensated for the cost they bear. WCs are charged for the social cost of emissions just as they charged for the opportunity cost of using scarce productive resources and capital goods (arrow 9).

Costs of production and use of capital assets

In a capitalist economy, capital assets are part of a company’s or an organisation’s balance sheet. In our accounting model, instead, we account for capital assets in separate accounting entities. We do this for two reasons, (1) we want to emphasize that capital assets are not owned by worker councils or organisations but belong to everyone in society, and (2) it facilitates the accounting of both the social cost of producing capital assets and the separate user right fees for the access to the same assets, which are set during the annual planning procedure to reflect opportunity costs. These two costs may very well differ.

In a participatory economy it is not privately owned companies, or capitalists or creditors who own and control capital assets, such as buildings, factories, production plants, machines, tools, or decide what investments society should make or who will get access to them. Instead, society’s productive resources belong to everybody. And consumer capital assets such as library buildings, hospitals and their equipment belong to a consumer council or federation.

At the lowest level, these sets of capital assets that are used for accounting purposes do correspond to today’s balance sheet of the individual worker councils and consumer councils, in the sense that they identify and record the assets that are used by the councils. However, in a participatory economy they constitute stand-alone entities that record both the assets’ historical acquisition cost and the user right fees that the councils pay for access to them. For purposes of analyses, the sets may be consolidated geographically in ever larger federations all the way up to the highest federation levels. Every defined industry and consumer federation may constitute a separate accounting entity for which the sets of assets are consolidated and monitored.

The production of new capital goods is handled and decided in a separate investment planning procedure that precedes the annual planning. When a set of manufactured capital goods is expanded, i.e., when a new capital good is acquired and added, the social cost of its production is charged to the set and will become an asset. Newly produced goods are financed through the Society Account, as indicated by arrow 14 in the flow chart, and the funds are forwarded to the worker council that produced the capital good, which will record a credit entry.

Then, when a worker council gets access to a productive capital asset, it is charged a fee for the right to use the asset as indicated by arrow 10 and 11, which is determined in the annual planning procedure. Note that this fee can very well be different from the actual social cost of production. Consumer councils and federations, however, are charged a fee that equals the assets annual depreciation of the original production cost plus a charged discount rate on the assets’ net book value, indicated by arrow 7. In both cases, the fees are forwarded to the Society Account and become part of Society’s total income.

Society’s income and its distribution

The Society Account records and tracks society’s income and how it is divided between consumption and investment. It provides a summary statement of the economy’s different sources of income and its allocation.

The total value of a participatory economy’s income in a year equals the sum of all paid and recorded fees for access to labour, capital assets, natural resources and land, and any operating surpluses or deficits from worker councils, and fees for emissions of harmful pollutants, but the latter are recorded in separate accounts as we have seen. The total income in a year will correspond to and be divided between the economy’s total consumption and investment.

Consumption, represented by workers’ income from work performed, consumers’ income from national benefit programmes, and costs for public service systems are all recorded as debit entries in the Society account. Funding of investment expenditures for productive capital assets, consumer assets, inventory, and non-productive and non-capital assets are also all recorded as debit entries.

Publications:

Anarchist Accounting. Accounting Principles for a Democratic Economy. Routledge 2021. Anders Sandström

Chapter 11 in Anarchism, Organization and Management. Critical Perspectives for Students. Routledge 2020. Martin Parker, Konstantin Stoborod, Thomas Swann

Start the discussion at forum.participatoryeconomy.org